What Covid can teach us about entrepreneurship?

Welcome to Plugging the Gap (my email newsletter about Covid-19 and its economics). In case you don’t know me, I’m an economist and professor at the University of Toronto. I have written lots of books including, most recently, on Covid-19. You can follow me on Twitter (@joshgans) or subscribe to this email newsletter here. (I am also part of the CDL Rapid Screening Consortium. The views expressed here are my own and should not be taken as representing organisations I work for.)

Covid-19 is a big multi-faceted shock. But these types of random events are grist to the mill for people trying to learn about economic forces. In other words, it often takes something out of the ordinary for us to learn about the ordinary.

I had been waiting for research along these lines and we have just got one new paper in my own field of entrepreneurship. The work by Cathy Fazio, Jorge Guzman, Yupeng Liu and Scott Stern examines new business starts in the US over the past 18 months. In particular, it looks at where businesses were started and how this was impacted by the three waves of stimulus in the United States. The NYT has a nice summary of the results.

The broad question of interest is not about Covid-19 but about what constrains entrepreneurial ventures. Is it, for example, a lack of opportunities? This has been a strong hypothesis in the past since new business starts tend to decline in recessions and increase in booms. Well, Covid-19 wasn’t your ordinary recession. The hit to economic activity was asymmetric. To be sure, there was a change in opportunities for some new businesses — opening up a restaurant or a physical store was not likely a good idea. But for services and online ventures the opposite was true.

The study shows that, in fact, would-be entrepreneurs seemed to take advantage of those shifting opportunities:

To be sure, there was an initial hit to new business starts but by the summer that had shifted.

But what about constraints? The biggest constraint is that people who become entrepreneurs often have to give up their day-job. Covid-19 forced a whole heap of that but also did that with a much stronger unemployment benefit cushion than usual. That gave people time to think about those opportunities and develop them.

“The idea that the pandemic has kind of restarted America’s start-up engine is a real thing,” said Scott Stern, an economist at M.I.T. and one of the authors of the research. “Sometimes you need to turn off the car in order to turn it back on.”

Of course, I don’t think he was suggesting that pandemics are a good thing per se. But it is the case that an enforced pause with time for reflection may well remove some barriers to taking what would otherwise have been a risk in life.

The other constraint on new businesses is, of course, liquidity. It costs money to start a new business — indeed, just the process of registering involves costs — not to mention holding inventory and paying employees (if you have them).

In a market economy, we aren’t actually supposed to have liquidity problems in starting businesses — at least in theory. This is because if something is a good plan for you, you should be able to take it to a bank and get a loan with a risk-adjusted interest rate and off you go. Of course, one thing we know is that loans for new business starts, especially when there isn’t a track record behind you, are few and far between. But it is hard to prove that.

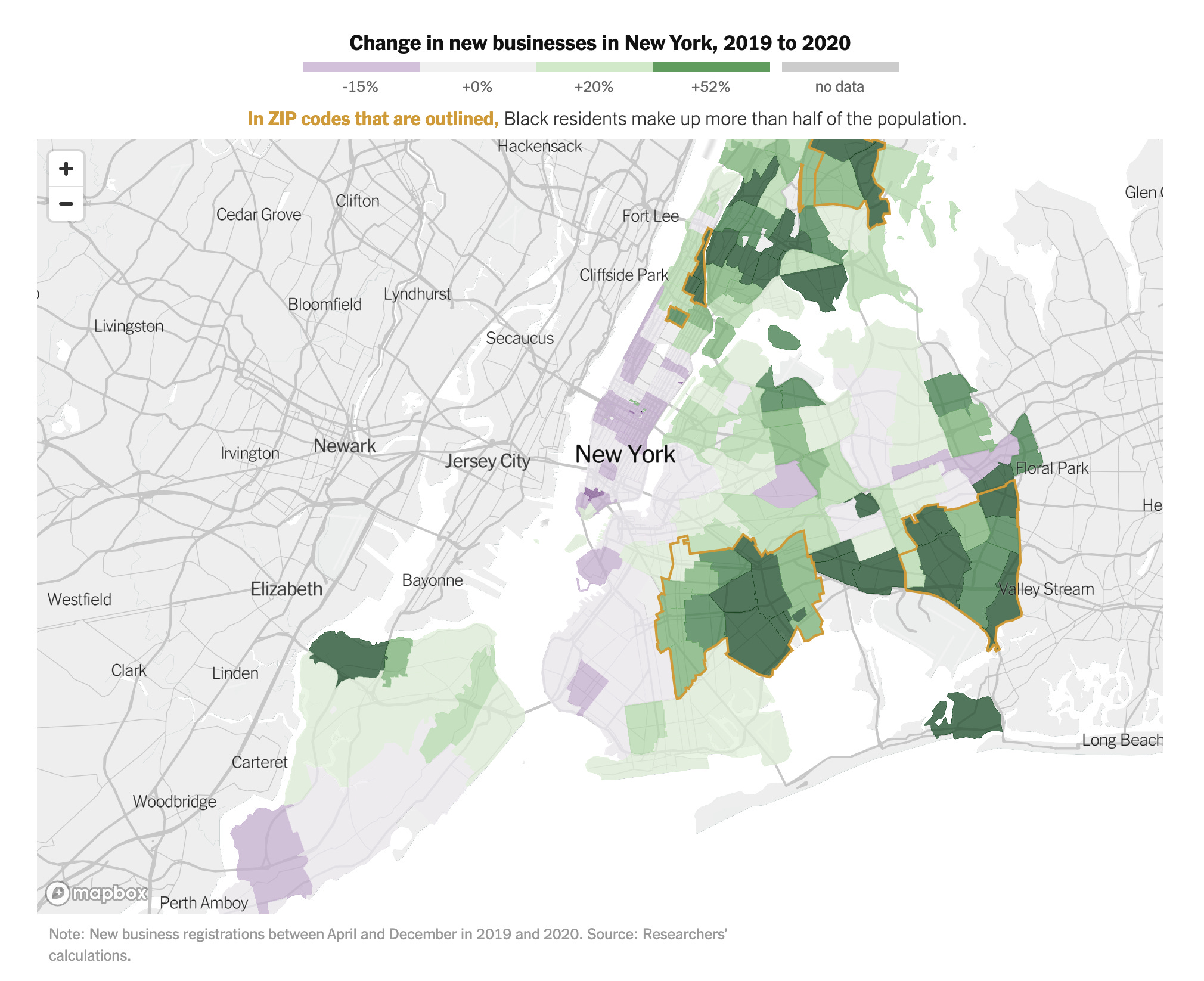

This is where the researchers turn to geography. Different neighbourhoods differ in terms of income but also in terms of other demographic factors — including, importantly, race. While you can’t tell the background of an entrepreneur from new business starts, you can tell where they are starting the business and make a guess as to the relatively likelihood they are low or high income or of one race or another.

The question is: what is driving liquidity issues? If you have low income and approach a bank for a loan, it is no real surprise to anyone if that loan doesn’t materialise. But it would be a real problem if race was a factor in that process.

We don’t know for sure from this study about that but interestingly, the paper finds that the biggest bump to new business starts following stimulus checks was in neighbourhoods with a higher proportion of black residents.

Is this good news? No, it is disturbing. On the face of it, it suggests that it was relatively difficult to get loans for new business starts in these neighbourhoods rather than other neighbourhoods. And that is controlling for income. Indeed, it was higher-median income black neighbourhoods that got the biggest bump.

This is evidence of discrimination in lending markets. There is good news, government stimulus money can overcome some of that. But one suspects this is the tip of a very deep iceberg.

Overall, what I think was going on was this. Covid-19 disrupted people’s lives. Some of those people took the time to pursue other opportunities. They weren’t necessarily doing it out of need — they need to start a business to survive — but instead just needed time and then some needed money. The money would otherwise be hard to come by but Covid-19 coincided with government checks which greased the wheels.

What we don’t know, of course, is the quality of these new business starts. But this team has extensive experience in thinking about how to assess that. It turns out that some quality variables are embedded in the choices people make when starting a business so perhaps we will have information on that soon.

Overall, however, the constraints to entrepreneurship are multi-faceted. What should worry us is that they are unevenly distributed. In other words, capital markets are working neutrally for some but are denied to others. How many? We will need more research to work that out.